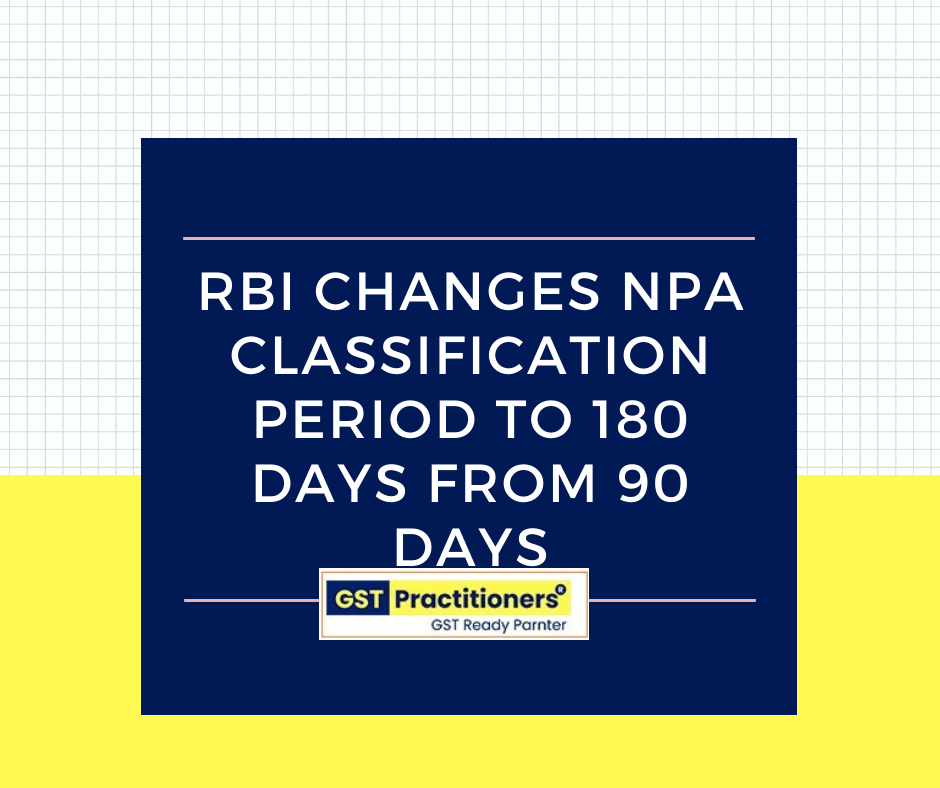

RBI has provided a relief to the standard bank accounts for Asset Classification and Provisioning. (Read Full Text)

The Reserve Bank of India (RBI) has decided to provide a relief to the standard bank accounts availing a loan moratorium between March 1 and May 31.

| RBI Governor’s Statement of April 17, 2020 announcing certain additional regulatory measures aimed at alleviating the lingering impact of Covid19 pandemic on the businesses and financial institutions in India, consistent with the globally coordinated action committed by the Basel Committee on Banking Supervision. In this regard, the detailed instructions with regard to asset classification and provisioning are as follows:

|

K.C.MAHATO is expert in GST Consultancy and has an experience of more than 10 years in Indirect tax , Direct Taxes and the accounting profession. He is also giving GST Practical Training to Students and SME Traders. He provide services that most effectively meet client needs. Her experience is concentrated in performing GST Laws & Practices and compliances of gst in a variety of industries.