Clarification issued on restrictions in availment of input tax credit available only 20% more of Invoices uploaded by the Supplier

Various issues relating to implementation of the Rule 36 (4) of CGST Rules 2017, have been examined and the clarification on each of these points is as under :

Issue No.1 : What are the invoices debit notes on which the restriction under rule 36(4) of the CGST Rules shall apply ?

Clarification : The restriction of availment of ITC is imposed only in respect of those invoices / debit notes, details of which are required to be uploaded by the suppliers under sub-section (1) of section 37 and which have not been uploaded. Therefore, taxpayers may avail full ITC in respect of IGST paid on import, documents issued under RCM, credit received from ISD etc. which are outside the ambit of sub-section (1) of section 37, provided that eligibility conditions for availment of ITC are met in respect of the same. The restriction of 36(4) will be applicable only on the invoices / debit notes on which credit is availed after 09.10.2019.

Issue No.2 : Whether the said restriction is to be calculated supplier wise or on consolidated basis ?

Clarification : The restriction imposed is not supplier wise. The credit available under sub-rule (4) of rule 36 is linked to total eligible credit from all suppliers against all supplies whose details have been uploaded by the suppliers. Further, the calculation would be based on only those invoices which are otherwise eligible for ITC. Accordingly, those invoices on which ITC is not available under any of the provision (say under sub-section (5) of section 17) would not be considered for calculating 20 percent. of the eligible credit available.

Issue No.3 : FORM GSTR-2A being a dynamic document, what would be the amount of input tax credit that is admissible to the taxpayers for a particular tax period in respect of invoices/ debit notes whose details have not been uploaded by the suppliers ?

Clarification : The amount of input tax credit in respect of the invoices / debit notes whose details have not been uploaded by the suppliers shall not exceed 20% of the eligible input tax credit available to the recipient in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub- section (1) of section 37 as on the due date of filing of the returns in FORM GSTR-1 of the suppliers for the said tax period. The taxpayer may have to ascertain the same from his auto populated FORM GSTR 2A as available on the due date of filing of FORM GSTR-1 under sub-section (1) of section 37.

Issue No.4 : How much ITC a registered tax payer can avail in his FORM GSTR-3B in a month in case the details of some of the invoices have not been uploaded by the suppliers under sub- section (1) of section 37.

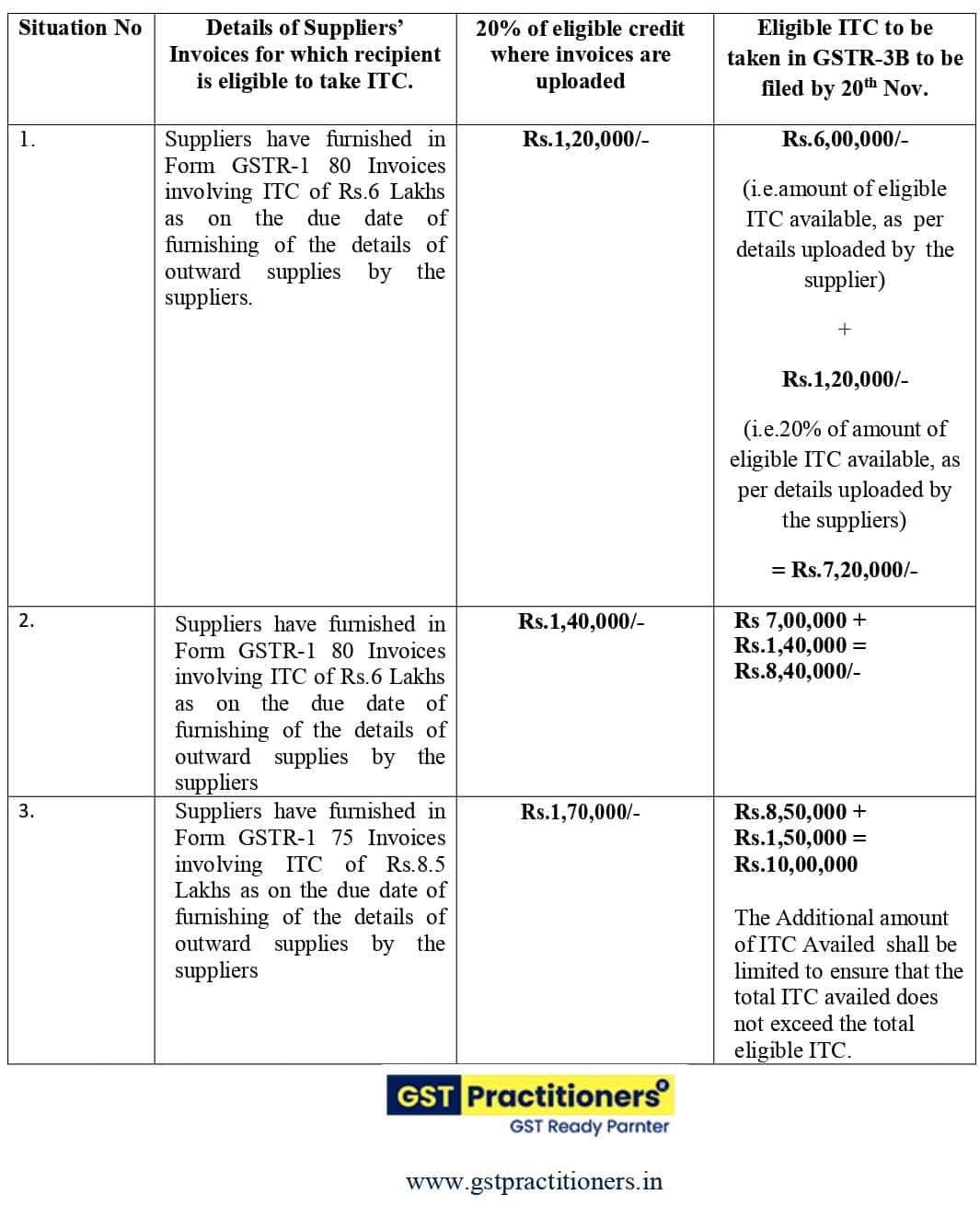

Clarification : Sub-rule (4) of rule 36 prescribes that the ITC to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37, shall not exceed 20 per cent. of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub-section (1) of section 37. The eligible ITC that can be availed is explained by way of illustrations, in a tabulated form, below.

In the illustrations, say a taxpayer “R” receives 100 invoices (for inward supply of goods or services) involving ITC of Rs. 10 Lakhs, from various suppliers during the month of Oct, 2019 and has to claim ITC in his FORM GSTR-3B of October, to be filed by 20th November’2019.

Issue No.5 : When can balance ITC be claimed in case availment of ITC is restricted as per the provisions of rule 36(4)?

Clarification : The balance ITC may be claimed by the taxpayer in any of the succeeding months provided details of requisite invoices are uploaded by the suppliers. He can claim proportionate ITC as and when details of some invoices are uploaded by the suppliers provided that credit on invoices, the details of which are not uploaded (under sub-section (1) of section 37) remains under 20 per cent of the eligible input tax credit, the details of which are uploaded by the suppliers. Full ITC of balance amount may be availed, in present illustration by “R”, in case total ITC pertaining to invoices the details of which have been uploaded reaches Rs. 8.3 lakhs (Rs 10 lakhs /1.20). In other words, taxpayer may avail full ITC in respect of a tax period, as and when the invoices are uploaded by the suppliers to the extent Eligible ITC/ 1.2. The same is explained for Case No. 1 and 2 of the illustrations provided at Sl.No.3 above as under:

Situation No. 1 :

“R” may avail balance ITC of Rs. 2.8 lakhs in case suppliers upload details of some of the invoices for the tax period involving ITC of Rs. 2.3 lakhs out of invoices involving ITC of Rs. 4 lakhs details of which had not been uploaded by the suppliers. [Rs. 6 lakhs + Rs. 2.3 lakhs = Rs. 8.3 lakhs]

Situation No.2 :

“R” may avail balance ITC of Rs. 1.6 lakhs in case suppliers upload details of some of the invoices involving ITC of Rs. 1.3 lakhs out of outstanding invoices involving Rs. 3 lakhs. [Rs. 7 lakhs + Rs. 1.3 lakhs = Rs. 8.3 lakhs]

K.C.MAHATO is expert in GST Consultancy and has an experience of more than 10 years in Indirect tax , Direct Taxes and the accounting profession. He is also giving GST Practical Training to Students and SME Traders. He provide services that most effectively meet client needs. Her experience is concentrated in performing GST Laws & Practices and compliances of gst in a variety of industries.